If you’re thinking of getting a mortgage, you probably already know the importance of having a decent deposit, good credit, and not being in huge amounts of debt.

You don’t need me to tell you how expensive houses are, and before lenders stump up that huge amount of cash, they’re going to want to make sure you can afford to pay it back.

Checking that your finances are in good order and that you don’t owe money left, right and centre is all par for the course, but lenders also want to check that you’re on the electoral roll, that you’re not applying for too much credit elsewhere, and that all your personal details add up before they approve you for a mortgage.

So far, so unsurprising, right?

But, did you know that there are some less obvious things that could stop you getting a mortgage?

My article takes a look at some of the weirder reasons your application for a mortgage could be declined.

Reasons such as:

1. Your Mortgage Application Is Declined Because Your Mates Think They’re Funny

Not in the general sense (we all know someone who mistakenly thinks that everything they say is hilarious after a few pints – spoiler alert: if you don’t that means it’s you. Stop it. No one’s amused.)

No, I’m talking about the ‘banter’ that has become popular when you pay money into someone’s bank account.

Not sure what I’m talking about?

Let me set the scene….

You and your mates are in Nandos and Tom’s forgotten his wallet. Again. You shout him the money (because you’re nice like that), and he says he’ll transfer it back to you tomorrow.

Sure enough, he’s true to his word, and when you check your account online the next day he’s paid you back.

However, instead of the accompanying note simply saying his name, or even ‘Nandos’, he’s typed in ‘Drug money’ or ‘sexual favours’ – no doubt thinking he’s incredibly funny and original.

The problem with this of course is that in the future, when a lender is taking a look at your bank statements, it can cause a bit of confusion.

It’s unlikely that they’re really going to believe you’re some sort of drug baron or well-priced gigolo, BUT, if these payments are regular – whether they’re coming in or going out – they ARE going to want to know more about where the money came from and why.

So, next time you’re tempted to transfer the 50 quid you borrowed off your mum with the note ‘arms deal’, think about how much of a moron you might look when you’re trying to do something incredibly adult and responsible, like get a mortgage.

2. Your Mortgage Application Is Declined Because Your Account Shows Gambling Transactions

Context matters here, but it’s a fact that if your bank statements show gambling transactions, you could be declined a mortgage.

Your weekly couple of quid on the lottery is unlikely to make a difference…nor is a large deposit made after a one-off casino trip win.

BUT, if you’re signed up to online betting sites and they’re showing up on your bank statements regularly, or large amounts of money are being withdrawn and paid in regularly because of gambling, lenders will see this as a huge red flag.

Why?

Well, put simply, lenders don’t like what they consider to be ‘risky behaviour’ – and gambling counts. If you have any concerns about a possible gambling addiction be sure to visit GamCare for support.

They might assume that someone who is gambling regularly has a problem – one that could lead to them making risky financial decisions, like taking out payday loans, and not being able to make their monthly mortgage payments.

3. Your Mortgage Application Is Declined Because You Are Sending Or Receiving Cash Gifts

You already know that lenders aren’t big fans of big spenders – especially if they can see that it’s leaving you short quite often. But surely giving someone a big sum of cash as a gift is different to splurging on yourself?

Not to lenders.

As far as they’re concerned it’s still extravagant spending, and even transferring someone £100 for their birthday could be a concern for lenders if it’s outside of your normal spending. The same goes for large cash gifts going IN to your account.

Just make sure that any amounts of cash going in or out of your bank account that might be seen as ‘unusual’ are easily explained, or it could affect you getting a mortgage.

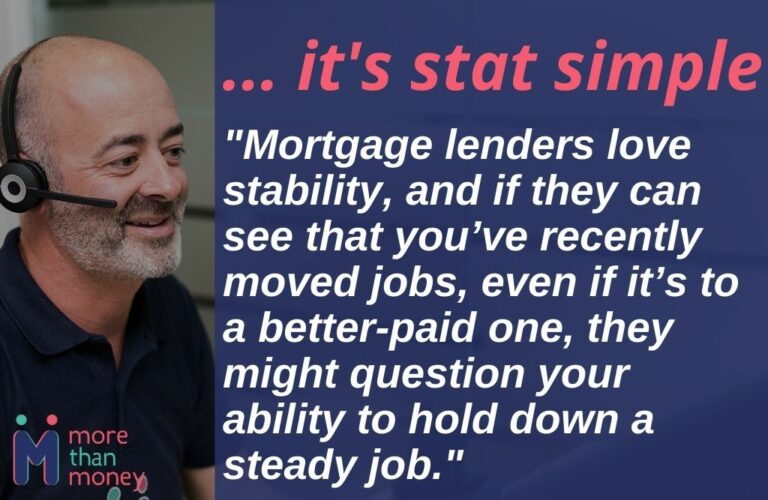

4. Your Mortgage Application Is Denied Because You Moved To A Better Paid Job

Surely being a better-paid job should have mortgage lenders chomping at the bit to approve your application. Why would you mortgage be declined?

It’s not the fact that you’re earning more money that’s the issue here, it’s the moving part.

Mortgage lenders love stability, and if they can see that you’ve recently moved jobs, even if it’s to a better-paid one, they might question your ability to hold down a steady job.

This can be just as true if you’ve JUST started working somewhere new after 25 years with the same company as if you’ve had 6 different employers in the last 6 months.

My advice if you’re thinking of a career change would always be to not make that move until AFTER you’ve applied for your mortgage.

Lenders LOVE to see a regular, steady paycheck, so ideally you want to have been in the same job for at least two years when you apply for a mortgage.

So, don’t be tempted to take that great-paying job the same week you apply for your mortgage – either hold off until you’ve been accepted, or put your mortgage dreams on ice for a couple of years

If you don’t, you could find your application is declined.

5. Your Mortgage Application Is Denied Because You Accidentally Omitted Information

Failing to disclose information when you apply for a mortgage is going to lead to you getting your mortgage application rejected and declined in one swift move.

And accidentally omitting information is going to have the exact same result.

Leaving out important information by accident is the same as deciding not to share something as far as mortgage lenders are concerned.

So, when you apply, make sure you’ve accounted for all of your income and spending, written down all your previous addresses correctly, and remembered how many kids you have…

Otherwise you could be back to square one.

So there it is folks, some weird and (un)wonderful ways that mortgage lenders might give you a big fat no when you go to them for a loan.

To be honest, your best bet is to speak to a broker before you start shopping around for mortgages. They’ll be able to help you get everything in order before you apply, and give you the best chance of being accepted.