How Much Deposit Do I Need For A Mortgage? Ah, the million dollar question…we hear people talking about saving for a deposit for a house all the time, but how much is that exactly?

You’ll be unsurprised to learn that when it comes to how much money you need to put down, the amount will depend on various factors.

We lightly touched on deposits in our article ‘WHAT IS A MORTGAGE?’ but now let’s look at that question in more detail.

In this article I discuss how much of a deposit you’ll need for a mortgage, with a focus on minimum deposits for the Government Help To Buy Scheme, Shared Ownership and Guarantor Mortgages.

Hold on tight folks, we’re going in…

How Much For A House Deposit

Long gone are the days of 100% mortgages – lenders just aren’t willing to take that risk any more.

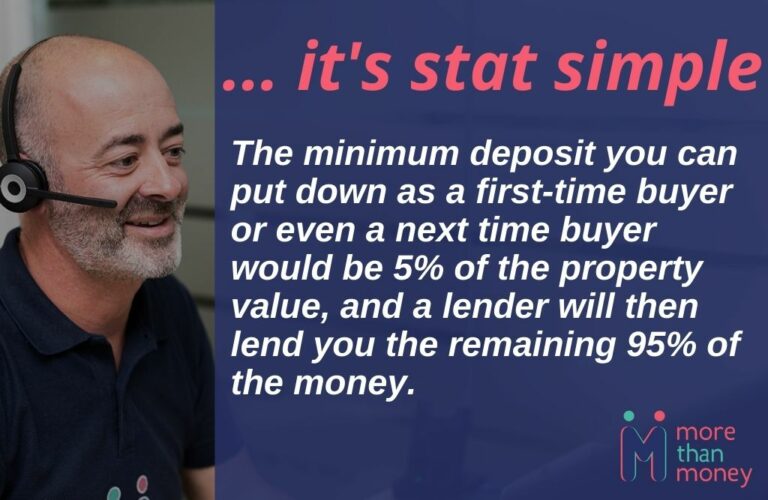

The minimum deposit you can put down as a first-time buyer or even a next time buyer would be 5% of the property value, and a lender will then lend you the remaining 95% of the money.

This is for residential mortgages only (the house you’re going to live in) as there are different criteria if you were looking to buy a property for investment – A Buy To Let (you can read our fab article on BTL mortgages for further information!)

Of course if you are able to put down more than 5% it would be an advantage to you.

And here’s why:

1. Your monthly repayments will be cheaper if you can put down a deposit of more than 5%

This sounds like an obvious thing to say, but the more money you have to put down, the less you need to borrow. And the less you borrow, the less you need to pay back each month.

2. You’ll be offered better mortgage deals if you can put down a larger deposit

If a lender can see that you have a larger deposit to put down they know they’ll have to lend you less money.

The less money they lend you, the less money they are risking, and therefore you’ll probably be offered a lower interest rate.

3. You have a better chance of being accepted for a mortgage if you can put down a big deposit

All lenders will look into your income and outgoings in order to determine whether you can afford your mortgage repayments.

If you only put down a small deposit it is more likely that your application could be declined.

This is because the lender looks much more closely at your financial situation as they are themselves taking a much higher risk in lending to you.

When a lender assesses the amount that they can lend you they all use what is called “affordability-based” lending.

What this means is that they will consider not only your regular income but also all of your other regular committed expenditures such as loans, credit cards, car finance, store cards, student loans, etc.

All lenders use their own affordability calculation criteria and therefore it’s always good to seek advice from a broker who can offer advice from the whole of the market rather than one or a small handful of lenders.

4. There’s less risk for you if you can put down more than 5% deposit

The more of the house you own, the less likely you are to fall into negative equity.

Negative equity is where you owe more on your mortgage than your property is worth (because the value of your house has dropped).

If you are in ‘negative equity’ it makes moving to a new house or switching mortgage very difficult.

See also Can I move my current mortgage to a new house?

But what if saving for a bigger deposit isn’t an option for you? I mean, it was hard enough sacrificing all those nights out and holidays just to save the 5% wasn’t it?! What can you do about it?

Turns out, quite a lot…

What Is The Government Help to Buy Scheme?

This is a scheme that has been designed to help those with a 5% deposit to get on the housing ladder and is available to first-time buyers purchasing a new-build property. https://www.ownyourhome.gov.uk/

The government will ‘top up’ your deposit with a further 20% of the value of the house. This is called a ‘Help to buy loan’ (basically, a loan from the government) which is interest-free for the first 5 years.

You must, however, start making interest payments from 5yrs onwards. So, although you will be making mortgage payments during that time – which will include interest – NO interest will be added to your Help to Buy loan.

The government effectively then has a 20% stake in your property and therefore if the property increases or reduces in value then their share does too!

The government’s share can however be paid back at any time in the future without any early repayment penalty.

A mortgage lender will lend you the remaining 75% which makes up the entirety of the property’s value.

What Are The Advantages Of The Government’s Help To Buy Scheme?

1. It is a quick way to get onto the housing ladder

2. You only need a 5% deposit

3. Your Help To Buy loan is interest free for the first 5 years

4. When the first 5 years are up you will get a competitive loan rate on the HTB element of your mortgage loan

The Disadvantages Of The Government’s Help To Buy Scheme

1. Your loan amount is not fixed so will increase with the value of your home

2. You are limited on this scheme to new build properties

3. You are limited to certain lenders

4. There is the danger of negative equity

5. Fees and terms are subject to change

The pros of a Help to Buy mortgage will probably outweigh the cons for those who love the idea of a new build and are intending to live there for a long time rather than sell in a few years and move on.

However there are other options open to you. Such as:

What Is Shared Ownership?

This is a scheme that allows you to buy a share of your home (between 25% and 75%), and pay rent on the share that you don’t own, which will be owned by a housing association.

This scheme is only open to first-time buyers, or those who used to own a home but can’t afford one any more.

Like the Help to Buy scheme you will need a smaller than average deposit, usually 5% of the amount of share that you are purchasing at the time.

What Are The Advantages Of Shared Ownership?

1. A quick way to get on to the property ladder

2. You can buy additional shares as and when you save money, and pay off more of your mortgage

3. Shared Ownership work out cheaper than renting

4. You can sell the property at any time and will benefit from any value increase on the share that you own since you bought it

What Are The Disadvantages Of Shared Ownership?

1. There might not be any shared ownership properties in the areas you want to live in

2. It can be difficult to buy more shares and increase the portion you own, because if the value of the property increases, the shares become more expensive.

3. You may have to pay a service charge to the housing association. This is an additional payment made towards the cost of maintaining any communal areas outside your home.

Ok so those are the options if you have at least SOME money to put down as a deposit.

But what about for those of us who know they can afford to pay a mortgage, desperately want to own their own home, but for whatever reason have nothing to put down at all?

Nothing you can do, right?

Wrong.

But it will involve you being reeeeeeally nice to mum and dad……. maybe ask them “how much deposit do I need for a mortgage” and they may get the hint!

What Is A Guarantor Mortgage?

We all know what the ‘G-word’ means, and often it fills people with dread, but if you know that you have the means to pay a mortgage, but no deposit, and have someone in your life who can help you out, this might be the scheme for you.

In short it typically means asking a close family member (in this instance it’s normally always mum and/or dad) “How Much Deposit Do I Need For A Mortgage?” and then getting them to agree to be named on the mortgage as your ‘guarantor’ and to cover your repayments if you miss them.

As you would expect there is A LOT to think about before either parties enter into this arrangement.

What Are The Advantages Of A Guarantor Mortgage?

1. A Guarantor Mortgage enables those who might not ever be able to otherwise to get a foot on the property ladder.

2. Also allows them to potentially borrow more as a result of the guarantor’s income.

3. It could put you in a position where you are able to purchase a more desirable property than if the loan amount were based on their own income.

See that all sounds lovely doesn’t it? No deposit and a great big beautiful house! Thanks Mum and Dad!

What Are The Disadvantages Of A Guarantor Mortgage?

1. If you don’t pay your mortgage, it is your guarantor who will be liable

2. Your guarantor will have to guarantee the mortgage payments with either their own property – which could be repossessed if you didn’t keep up your mortgage repayments, or their savings – which the lender would hold in an account until you have paid off a percentage of your mortgage.

3. It could put a strain on relationships. Some parents might feel they have the right to know more about your finances and how you spend your money now that their home is at stake if you fail to keep up with repayments.

Is a jealous sibling going to start giving you grief? How does your partner feel about your parents’ involvement – or vice versa? What would the consequences be if you split? All things to think about.

If we haven’t fully answered “How Much Deposit Do I Need For A Mortgage” or you have any more related questions feel free to speak with me directly. We’re dedicated to finding the best mortgage product for you, whatever your circumstance, so why not get in touch – we’d love to help.

Your home may be repossessed if you do not keep up repayments on your mortgage.